July 2015, Vol. 242, No. 7

Web Exclusive

Ethanol Production May Be Approaching 'Blend Wall'

It’s onward and stubbornly upward for the U.S. ethanol industry, which shows little sign of slowing after a record year in 2014.

Weekly ethanol production matched its record high in the first week of June, equaling output from the week ending December 19, 2014. At 992,000 bpd, production is up 20,000 bpd from last week and more than 100,000 bpd since the beginning of May.

Federal mandates like the Renewable Fuel Standard (RFS) – enacted in 2005 and expanded in 2007 – have turned the fuel additive into a $40 billion industry. Buoyed by high exports – up 3% from 2013 – ethanol production totaled more than 14.3 billion gallons in 2014. For its part, corn also had a record year with production reaching 14.2 billion bushels.

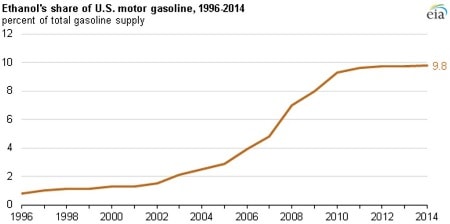

Currently, fuel ethanol accounts for about 10% of the total volume of finished motor gasoline consumed, though there are questions surrounding just how much higher that share can go. Put simply, there are limitations, both legal and practical, on the amount of ethanol that can be blended into the gasoline supply.

This limit, or “blend wall,” is a factor of ethanol’s lower energy content, higher consumer cost, and the market limitations surrounding higher blends like E85. As a result, and despite its rapid growth, ethanol use has fallen behind the RFS targets – a gap that is expected to widen as gasoline consumption declines toward 2020.

In an effort to address this plateau and reestablish realistic targets, the Environmental Protection Agency – in May – proposed a set of changes to the RFS for 2015 and 2016. Toward 2016, the proposal calls for a 9 percent increase in the use of renewable fuels by volume. However, targeted growth for conventional corn ethanol is lower at only 5%.

Instead, the EPA is pushing advanced biofuels, raising the target more than 20% by 2016. The proposal is due to be finalized in November.

Advanced biofuels like cellulosic ethanol – made from corn husks, stalks, other waste residues, and native grasses – have long been seen as the RFS’ endgame, though their development has lagged far behind expectations. 2014 was very much a breakthrough year for the industry, which saw the opening of the first commercial-scale plant. Early entrants like Abengoa, Poet, and Royal DSM have largely avoided the kinds of losses felt by their oil industry counterparts.

Still, moving forward, there are more questions than answers. While the EPA proposal addresses any lingering uncertainty regarding RFS support, it does little to solve the market-based problems surrounding both conventional and cellulosic ethanol.

Domestically, much of the nation’s automotive fleet and fueling infrastructure cannot support higher ethanol blends like E15 and E85, nor is there demand for them among consumers.

Moreover, the fuel additive’s environmental efficacy is questionable at best. A recent study from Environmental Working Group (EWG) suggests the carbon intensity of corn ethanol is 20% greater than standard gasoline. EWG estimates that the production and use of E10 in 2014 resulted in 27 million tons more carbon emissions than if U.S. drivers had burned straight gasoline.

All told, exports present the most compelling – and necessary – opportunities for growth. Global demand is trending up, but a strong U.S. dollar may favor lower cost producers like Brazil. Securing markets abroad will be key as bigger players like Archer Daniels Midland and Green Plains Energy face shrinking margins.

The financial weight and political significance suggest corn ethanol isn’t going anywhere. However, barring drastic changes to the RFS, it’s gone about as high as it can go. Of course, biofuels are far from played out; one need only look toward biogas – and its multitude of uses – to discover that the industry still has much to offer.

Comments