August 2019, Vol. 246, No. 8

Mexico Spotlight

Mexico Looks to Expand Pipelines, Develop Own Reserves

By Nicholas Newman, Contributing Editor

Mexico’s rapid growth of demand for electricity over the last decade happily coincided with burgeoning supplies of cheap shale gas in nearby Texas. This Mexican demand and Texan abundance drove a boom in cross-border pipeline construction which continues to this day.

Mexico’s own declining gas output helped encourage liberalization of the energy market in 2013, allowing both the private and public sector to seize the opportunity provided by cheap gas supplies to begin building gas power stations and new gas pipelines, a trend which was subsequently reinforced by the government’s commitment to meet its Paris Accord targets for the reduction of greenhouse gas emissions.

The results are stunning. In 2017, Mexico was the world’s seventh-largest consumer of gas at 8.7 Bcf/d, and imports of U.S. gas met half of Mexico’s gas consumption needs.

Pipeline gas imports from the U.S. exceeded 5 Bcf/d in July 2018, according to the EIA and account for roughly 85% of Mexico’s natural gas imports with the remaining 15% arriving in the form of LNG exported from Sabine pass to LNG re-gas terminals at Altamira on the east coast and Manzanillo and Costa Azul on the west coast.

Mexico was an early beneficiary of cheap American shale gas from Texas and New Mexico and the burgeoning supply of oil, and associated gas from the Permian Basin underpins forecasts of rising U.S. gas exports to satisfy around 70% of Mexico’s gas needs in 2022.

Import Drivers

Output of natural gas in Mexico has declined each year since 2010, despite abundant reserves. This is largely due to the halving of Pemex, the state oil company’s annual investment budget from $12 billion in 2014 to just $6 billion in 2017 and lack of access to modern technologies.

The 2013 energy market reforms opened the state power sector to private investment which together with the climate agenda hastened the shift from coal and oil for heat, power and transport, toward cleaner gas and low carbon energy sources of wind and solar power. Gas power capacity increased from only 2 GW in 2015 to 15 GW in 2019. In 2017, gas power generation supplied 53% of the country’s power needs.

Growth in Mexico’s energy intensive industries, particularly the chemical, plastics and metals sector, alongside a growing middle class, saw electricity demand rising by 2.3% a year.

Gas was the beneficiary of industrialization and increased demand from the residential and commercial sectors, facilitated by a boom in pipeline construction, bringing the total number of cross-border gas pipelines to 10 and extending the domestic gas pipeline network to over 18,074 miles to bring gas to industrial cities in the north and central Mexico.

Pipeline System

In the last decade, national company Cenagas, owner and operator of the bulk of Mexico’s gas pipelines, financed a pipeline building boom to bring Texas gas to markets in the central, western, southern regions, as well as cities and towns that include Gómez Palacios and Torreón.

In addition, some pipelines have been built on a design, build and operate basis in joint ventures between Cenagas and foreign companies, including TransCanada and Sempra. Cenagas plans to extend the gas network to the western coastal states of Baja California Sur, Guerrero, Nayarit, Oaxaca and Chiapas, as well as the eastern coast to Quintana Room on the Yucatan Peninsula.

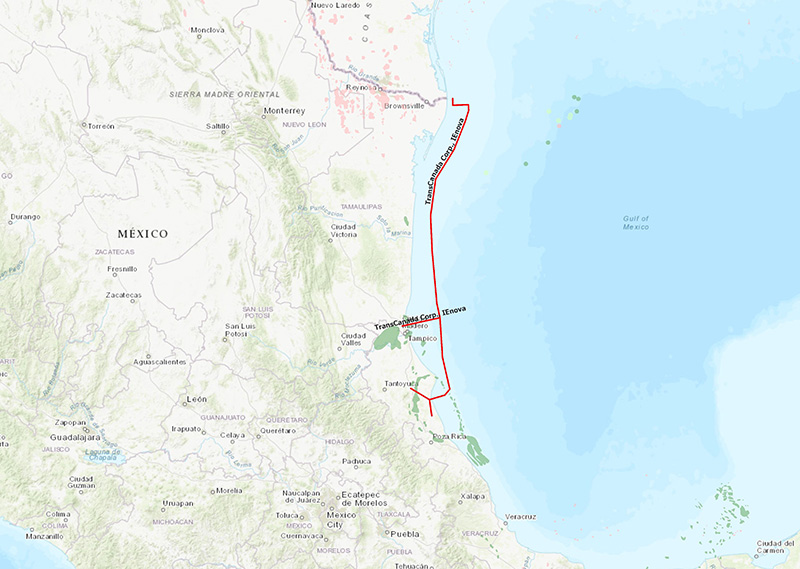

Foreign pipeline developers, including TransCanada, Enbridge and NuStar Logistics LP, are also developing new capacity on behalf of state power utility CFE, which on completion will allow every major population and industrial center in the country to have direct access to Mexico’s national pipeline network.

However, pipeline construction has not been entirely free of corruption, extortion and opposition. In late 2018, TransCanada halted construction of two natural gas pipeline projects in Hidalgo, Central Mexico, worth more than a billion dollars. An open letter from TransCanada’s Mexican subsidiary published in several Mexican newspapers read:

“The social and legal uncertainty that prevails in this state makes the continuity of our investments impossible. On multiple occasions, social groups have made irrational requests that border on extortion and have performed acts outside the law.”

Two recent projects that have met with success:

The $3.1 billion Sur de Texas pipeline is a cross-border pipeline carrying Eagle Ford gas from the gas hub of Brownsville, Texas, to the Mexican port city of Veracruz. Completion of the Mexican section in February 2019 enabled 2.6 Bcf/d of natural gas to be sent into Mexico.

The 372-miles, 42-inch La Laguna-Aguascalientes is a CFE-sponsored natural gas pipeline in Mexico, designed to supply 1.19 Bcf/d of gas to the company’s power-generation plants in the states of Durango, Zacatecas and Aguascalientes, as well as other portions of central and western Mexico. The pipeline will interconnect with 42-inch, 262-mile El Encino-La Laguna pipeline, which carries gas from Waha Hub in Texas to northwestern Mexico and with the 42-inch, 220-mile Villa de Reyes-Aguascalientes-Guadalajara gas pipelines.

Additionally, two refined products cross-border pipelines have received approval. The Howard Midst Ream’s Dos Aguilars will carry refined products, 287 miles from Corpus Christi, Texas, to Monterrey, Mexico.

Its four, 12-inch sections make up the Border Express pipeline from Corpus Christi to Laredo, Texas, the Borrego from Laredo to the international border crossing (151 miles), then from the border to Nuevo Laredo, Mexico, and Politico del Norte from Nuevo Laredo to Monterrey (136 miles).

The NuStar Logistics and Pemex refined products cross-border pipeline proposal is envisaged to run parallel to an existing line carrying NGLs from Edinburg, Texas, to Pemex’s Burgos gas plant near Reynosa, Mexico. This 46-mile pipeline will be 10-inches in diameter.

The NuStar and Pemex

cross-border pipeline is

envisaged to run parallel to an existing line carrying NGLs from Edinburg, Texas,

to Pemex’s Burgos gas plant near Reynosa, Mexico. This 46-mile pipeline will be 10-inches in diameter.

Outlook

The new government under President Andres Manuel Lopez Obrador has indicated that it wants to reduce dependence on U.S. gas and has instructed Pemex to develop 20 oil and gas fields, in and around the Gulf of Mexico, to boost domestic output by 50% over the next six years.

Mexico also has huge shale gas reserves in the north, along the Rio Grande Valley, next to the Texas border and in the southeast in Veracruz and Macuspana basins.

Pemex has received permission to drill wells in four blocks in the northwestern part of Veracruz. Allowing fracking to access even a small portion of this, could allow Mexico to reduce its dependence on imported gas quickly. However, much of Mexico’s shale gas prospects lie in regions with poorly developed supporting transportation, communications and security infrastructure.

For the next decade, growing demand for electricity will be met by natural gas and renewable energy and facilitated through further expansion of the Mexican gas grid. Imports of gas from the U.S. are set to continue to rise until the early 2020s, notwithstanding a recovery of oil and gas exploration by Pemex. P&GJ

Comments