August 2021, Vol. 248, No. 8

Features

2021 Midyear International Outlook: Pipeline Construction & Market Trends

By Jeff Awalt, Executive Editor

As global markets claw their way back from the 2020 pandemic trough and energy demand continues to rise, oil and gas producers remain largely committed to fiscal restraint, prices have risen to multi-year highs and storage has yet to recover from historic lows.

Along with projected higher demand, these trends have brightened the outlook for the global midstream sector and raised expectations for ongoing recovery over the next few years, with construction activity weighted more heavily toward natural gas infrastructure. The speed and extent of that recovery is still uncertain, however, and is likely to vary widely from one regional economy to the next.

Market Drivers

Global gas demand is expected to rise by 3.6% in 2021 before easing to an average growth rate of 1.7% over the following three years, according to the International Energy Agency’s (IEA) latest quarterly Gas Market Report published in early July. A strong rebound in 2021 from last year’s decline is expected to lift demand above pre-Covid levels, followed by more moderate increases through 2024, IEA said.

Natural gas demand growth in 2021 mostly reflects economic recovery from the Covid-19 crisis, but it’s set to be driven in the following years in equal proportions due to both economic growth activity and by the ongoing shift from more polluting fuels such as coal and oil to natural gas in sectors such as electricity generation, industry and transportation, IEA projects.

“The rebound in gas demand shows that the global economy is recovering from the shock of the pandemic and that gas is continuing to replace more emissions-intensive fuels,” said Keisuke Sadamori, IEA director of Energy Markets and Security.

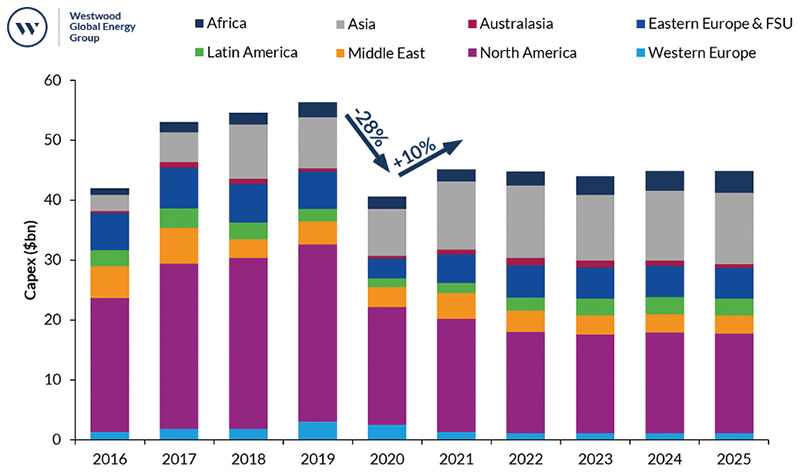

Total worldwide capital spending on pipeline installations is projected to increase about 10% this year after plunging nearly 30% in 2020, according to Westwood Global Energy Group, with North America, Asia, Eastern Europe and the former Soviet states accounting for about three-quarters of all Capex for new pipeline construction in its 2021-2025 forecast period.

“Improving sentiment and outlook for commodity prices is expected to help projects progress through to completion, as well as boost demand for new installations in regions, where increases in production capacity will require new pipeline infrastructure,” Westwood predicts.

LNG Upside

A recent report by investment firm Morgan Stanley highlighted the spike in LNG demand as yet another indication of economic recovery and future infrastructure demand.

“Global demand has continued to surprise to the upside, most notably in China, and has recently been boosted by a hot start to the summer,” the firm wrote in its June 29 update. “This surging consumption comes amidst a backdrop of lingering supply outages. The combination of these factors has continued to tighten the LNG market even more rapidly than our expectations.”

Longer term, Morgan Stanley said it continues to see an upcycle for global LNG markets through 2025, with demand set to grow at two times the rate of supply, “leading to a capacity shortfall by 2023.” This could prove to be a positive trend for related construction in the United States and other LNG-exporting nations.

Growing demand for LNG and related natural gas infrastructure is a key driver of current and planned pipeline construction worldwide. Gas infrastructure accounts for 66% of projected new pipeline installations through 2025, Westwood said, while joining others in warning of ongoing downside risk to their forecasts.

REGIONAL UPDATES

Africa

Oil remains the primary fuel in Africa, and there are a number of sizable crude oil pipelines in various planning and construction stages. But with nearly 500 Tcf (14 Tcm) of proven natural gas reserves, there is growing opportunity for natural gas to displace oil in Africa – especially in the power generation sector, with South Africa leading demand. In addition to regional demand, an abundance of natural gas has fueled a growing LNG export market.

“This pipeline project can be a core of bigger deployments,” said Ugandan President Yoweri Museveni, who added that the EACOP corridor could be used to build another pipeline to ship natural gas from Tanzania and Mozambique to consumers in Uganda, Rwanda, Congo and other countries in the region.

Nigeria National Petroleum Corporation (NNPC) has plans to construct the biggest natural gas pipeline in that country’s history – a $2.8 billion, 384-mile (614-km) project from Ajaokuta to Kano. The 40-inch (1,016-mm) line will transport 3.5 MMscf/d (98,882 cm/d) from multiple gathering projects in southern Nigeria, resulting in the establishment of a connecting network between its eastern, western and northern regions.

Tanzania and Kenya are constructing a 345-mile (558-km) gas pipeline between Tanzania’s Dar es Salaam and Tanga and on to Mombasa, in Kenya’s coastal city of Mombasa. The project, which is being developed under a contract by China Petroleum Technology and Development Corp.

A group of 15 West African countries also is studying the feasibility of extending the 420-mile (678-km) West African Gas Pipeline, owned by the JV West African Gas Pipeline Co. (Wapco). Launched in 2010, the pipeline connects the Escravos-Lagos pipeline at Nigeria Gas Co.’s Itoki export terminal to Takoradi in Ghana, with laterals to points in Ghana, Benin and Togo.

Uganda has held promise as an oil producer since discovering reserves estimated at 6 billion barrels in the Albertine Rift Basin, near its border with the Democratic Republic of Congo, in 2006, and government leaders have begun taking steps toward the infrastructure necessary to bring those reserves to market. In April of this year, Uganda, Tanzania and oil firms Total and CNOOC signed agreements that will kickstart the construction of the $3.5 billion East African Crude Oil Pipeline (EACOP).

Asia Pacific

Almost half of IEA’s projected worldwide increase in natural gas demand through 2024 comes from the Asia Pacific region, where China’s appetite for natural gas and LNG imports continues to lead the region’s fast-growing development of natural gas infrastructure.

China – the region’s largest energy consumer and the first in and out of the pandemic shutdown is making an outsized contribution in rising global LNG demand forecasts.

“China has been the biggest outlier to the upside,” Morgan Stanley wrote of its updated projections, with LNG imports up 27% during the first five months of the year, compared with the same period of 2020.

Among recent projects, China Oil & Gas Piping Network Corp. (PipeChina) has begun building a $1.31 billion (8.5 billion yuan), 257-mile (414-km) pipeline to transfer natural gas from a 2.2 million-tonnes-per-year LNG terminal in Tianjin to Xiong’an New Area, Hebei Province. The pipeline will include interconnections for Gazprom’s Power of Siberia pipeline, which began delivering natural gas to China in late 2019, as well as domestic pipelines delivering gas from the Xinjiang Autonomous Region, PipeChina said.

The 1,865-mile (3,000-km) long Power of Siberia pipeline transports gas from the Chayandinskoye and Kovytka fields in eastern Siberia, to Heilongjiang, which borders Russia, and goes onto Jilin and Liaoning, China’s top grain hub. Flows via the Power of Siberia are expected to gradually rise to 38 Bcm/year in 2025, potentially making China Russia’s second-largest gas customer after Germany.

Gazprom last year announced a feasibility study for a proposed Power of Siberia-2, which would deliver up to 50 Bcm/year of natural gas to China by way of Mongolia. Gazprom showed plans during an investor event to launch the pipeline in 2030 but said the timing of the project will depend on the pace of global and regional economic recovery.

After partial start-up last year, China expanded its flow of natural gas this year to an estimated 2 Bcm/year through a newly laid 367-mile (591-km) pipeline in the central province of Hunan. This provincial section, which the Chongquing Oil and Gas Exchange said is designed for an ultimate capacity of 9 Bcm/year, is part of the massive, 6,693-mile (4,159-km) Xin-Yue-Zhe national pipeline project that connects gas production in the northwest region of Xinjiang to the southern manufacturing hub of Guangdong province.

China also approved construction last month of a natural gas pipeline connecting the northern provinces of Shanxi and Shaanxi, with a total investment of $54.8 million (354 million yuan), according to the National Development and Reform Commission (NDRC). The 21.3-mile pipeline, which will be built by Quinjin Natural Gas Co., is designed for annual capacity of 3.3 Bcm.

In India, a significant expansion of natural gas pipeline infrastructure is underway as it seeks to double the share of gas in its energy mix to 15% by 2030. Toward this goal, companies are investing $60 billion in a network to expand LNG import facilities in the west and build pipelines connecting them to every state before the current government’s term ends in mid-2024, according to India’s energy minister.

Among the major projects currently under construction by India’s biggest gas utility, Gail Ltd is building the 1,660-mile (2,660-km) Urja Ganga pipeline project to connect the eastern states of Bihar, West Bengal, Jharkhand and Odisha, with a capacity of 16 MMscf/d (452,034 MMcm/d) – an amount equal to roughly 10% of India’s total daily consumption. Gail hopes to bring the system online by the end of this year.

Europe

With energy consumption plateaued in Europe in recent years, natural gas continues to take taking a growing percentage of the mix, sparking political conflict over the region’s reliance on Russian energy and a market-share showdown between Russian pipeline gas and U.S. LNG imports.

European gas demand during the second quarter of 2021 was on pace for an estimated 20% gain over the same period of 2020, Morgan Stanley said. On the supply side, LNG imports have recently fallen below 2019 levels as cargoes were being diverted to Asia and Latin America, according to the firm’s Global Gas & LNG report. Russian import volumes have remained below pre-pandemic levels this year, while Norwegian gas supplies have lagged year-over-year due to outages.

European gas storage has begun to fill at a rate near the historical average, Morgan Stanley reported, but was still 14% below normal at the end of June.

As natural gas demand in Europe has grown largely due to coal-to-gas switching, so has the need to expand or replace aging natural gas infrastructure. That scenario becomes more complex as a drive toward broader commercial adoption of hydrogen prompts debate over the construction of new hydrogen pipelines vs. the conversion of natural gas lines, or some combination of the two.

Much of the European pipeline construction in recent years has been driven by either the construction of major Russian gas pipelines across the Baltic and Black seas or the construction of new pipelines by European Union countries who fear overreliance on Russian gas imports.

A long-running conflict over the nearly completed construction of Gazprom’s Nord Stream 2 pipeline appears to have been effectively resolved within a few months of U.S. President Joe Biden’s inauguration when Secretary of State Antony Blinken said the United States would no longer pursue sanctions against companies involved in the project. A Congressional challenge was still afoot, and the U.S. and Germany said they hoped to resolve the dispute by the end of this month, but the project is near completion.

Nord Stream 2 runs alongside the first Nord Stream pipeline, which began operations in 2011, from Russia’s Baltic coast to Germany by 2019. Russia has said it expects to finish construction by the end of the year, concentrating about 70% of Russian gas exports to Europe into a single route and rendering a number of existing pipelines obsolete.

Among those pipelines are several that run through Ukraine, which stands to lose up to $2 billion in annual transit revenues if gas is diverted away by Nord Stream 2. German Chancellor Angela Merkel said before a recent White House meeting with President Biden that Ukraine can be confident Germany and EU will guarantee its status as a transit country for Russian gas even after the Nord Stream 2 pipeline has opened.

Among the ongoing pipeline construction projects aimed at diversifying Europe’s natural gas sources, Polish and Danish gas grid operators Gaz-System and Energinet are developing the Baltic Pipe, a 528-mile (850-km) bidirectional project that gives Denmark, Poland and Sweden direct access to Norway’s North Sea gas and moves Poland closer to its goal of becoming eastern Europe’s gas hub.

The project will deliver up to 353 Bcf (10 Bcm) per year upon expected completion in 2022 at a projected cost of $1.88 billion. Poland and Denmark are financing construction, along with a $243 million contribution from the European Commission. Construction of the project stalled in Denmark earlier this summer for its Environmental Protection Agency to study whether the project may harm breeding grounds for protected mice and bat species. Energinet said it will not resume construction work until permits are approved.

Construction of the Baltic Connector, which links Finland’s gas network with the Baltic states, came online in 2019, providing a key piece of a planned system that will eventually make it possible for all Baltic states to import gas from Poland. The Gas Interconnection Poland–Lithuania (GIPL), a bidirectional gas pipeline linking the Baltic states with Poland, is expected to add to the network in late 2021.

Among numerous hydrogen projects under consideration in Europe, Energinet and the Netherlands’ Gasunie published a technical pre-feasibility study this year for transporting hydrogen via a 217- to 279-mile (350- to 450-km) pipeline from Esbjerg or Holsetebro, Denmark, to Hamburg, Germany.

Middle East

The Middle East has continued to build out its natural gas and LNG infrastructure following large discoveries in the Eastern Mediterranean during the past decade. Some governments also remain focused on the construction of new crude oil pipelines, although the pandemic has slowed progress of at least one major project.

The Iraqi oil ministry in December announced the completion of its pre-qualification process for construction of an estimated $18 billion oil pipeline that would carry 1 MMbpd of oil from Basra through the Jordanian port of Aqaba and across the Red Sea to Egypt.

The first phase of the project would be constructed in Iraq across a 435-mile (700-km) stretch between Rumaila and Haditha. Developers delayed the May 2020 deadline for technical offers for the project, known as the Iraq Jordan Export Pipeline (IJEP), due to COVID-19. Energy ministers in both Jordan and Iraq have reiterated their support for the project but have yet to reschedule a meeting with interested bidders.

In neighboring Iran, President Hassan Rouhani launched a 620-mile (1,000-km) crude oil pipeline from Goreh to Jask in June, noting its strategic value as a secondary export route “whenever the Strait of Hormuz faces danger.” About 20 MMbpd of oil passes through the narrow strait, making it vulnerable to military blockades.

North America

North America was in the midst of significant pipeline expansion before the pandemic shutdown and, accordingly, suffered the greatest regional decline in new construction activity over the past year and a half. The construction downturn was not entirely driven by economic conditions, however, as legal challenges caused construction delays for projects such as PennEast and Line 5 and cancellations of major projects including the Atlantic Coast and Keystone XL pipelines.

North American oil and gas demand and pricing improved in the first half of 2021, prompting some energy firms to say they plan to boost spending in the coming months after cutting expenditures over the past two years. Any near-term spending increases will be measured, however, as most firms continue to focus on boosting cash flow, reducing debt and increasing shareholder returns rather than adding output.

The midyear consensus among market analysts suggests extra spending may only replace natural declines in well production, rather than boosting output, exacerbating the capacity glut. U.S. crude oil production is expected to fall by 210,000 barrels per day in 2021 to 11.1 MMbpd, the U.S. Energy Information Administration (EIA) said in July.

The outlook for natural gas pipeline and LNG infrastructure appears somewhat brighter, with a number of North American projects including Canada LNG and the related 416-mile (670-km) Coastal GasLink pipeline moving forward, and additional U.S gas pipelines in the planning stages.

Natural gas prices for the second half of 2021 rallied more than 25% during May-June, spurred by higher gas demand for electricity production due to an unseasonably hot start to the summer, strong exports to Mexico, increased U.S. industrial demand and lower hydropower generation in the Western United States caused by below-normal reservoir levels.

“Heading into next year, we expect (U.S.) associated gas production to increase with rising basin level gas-oil ratios and additional oil-directed drilling activity, particularly from private producers,” according to the Morgan Stanley forecast. “We also expect higher prices to incentivize modest dry gas production growth to resume in the Haynesville and Marcellus” by the second half of 2021.

Among projects aimed at domestic natural gas markets, Enbridge said in April that it is moving ahead with upgrades to its pipeline network serving the U.S. Northeast from the Appalachian Basin. The first phase, at an estimated cost of $28 million, will include a connection to a UGI Utilities facility in Pennsylvania and a compression boost to move an additional 18 MMcf/d on its Texas Eastern system. Similar links are to be built for other regional customers in the second phase of the program, Calgary-based Enbridge said.

Enbridge also plans to start construction this year on a tunnel beneath the Straits of Mackinac, connecting Lake Huron and Lake Huron, as part of its Line 5 replacement project. The proposed tunnel, which has faced multiple legal challenges, would rehouse a 4-mile (6.44 km) stretch of the aging 540,000-bpd oil pipeline that currently runs along the lake bed.

An Enbridge project to replace its Line 3 pipeline scored a court victory in June when the Minnesota Court of Appeals affirmed a state regulator’s decision that there is sufficient need to replace the line. Functional capacity of the 1960s-era pipeline, which delivers crude from Alberta’s oil sands to U.S. Midwest refiners, has been constrained by age and corrosion. Replacing it will allow Enbridge to roughly double its capacity to 760,000 bpd.

Also in June, the U.S. Supreme Court ruled in favor of a consortium of energy companies seeking to seize land owned by the state of New Jersey to build the federally approved PennEast Pipeline, a 116-mile project designed to transport 1.1 Bcf/d of natural gas from the Marcellus shale formation in Pennsylvania to customers in Pennsylvania and New Jersey. PennEast expects the first phase of the $1.2 billion project to begin service in 2022, with completion of the second phase into New Jersey in 2023.

In the U.S. Midwest, Navigator CO2 Ventures plans to build a 1,200-mile (1,931-km) carbon capture pipeline system designed to capture and store 12 million tons of CO2 per year. The project, which would span five states, is supported by the BlackRock Global Energy & Power Infrastructure Fund, and Valero is the anchor customer, Navigator said. Navigator a binding open season for the project in June.

WBI Energy recently received U.S. Federal Energy Regulatory Commission (FERC) approval for construction of its proposed North Bakken Expansion Project – a 250 MMcf/d pipeline spanning 82 miles of western North Dakota, along with a new compressor station and associated infrastructure. WBI targets completion of the $260 million project by the end of the year.

FERC also approved Enable Midstream’s 134-mile (216-km) Gulf Run natural gas pipeline in Louisiana, which would transport gas to the Qatar Petroleum/Exxon Mobil Golden Pass LNG export plant under construction in Texas. The first liquefaction train at Golden Pass is expected to enter service in 2025.

Summit Midstream has started construction of the 134-mile (217-km) Double E pipeline and estimated $425 million project to transport natural gas from the Delaware Basin to various delivery points in and around the Waha Hub in West Texas. The company said it has received $175 million of commitments from three commercial banks to finance the development.

Russia & CIS

Russia’s growth strategy for natural gas pipeline exports has targeted Europe since the 1950s, but it is expanding its flow of gas to the east by targeting China’s growing energy demand.

Last year, state-owned giant Gazprom completed construction of the 1,865-mile (3,000-km), Power of Siberia pipeline, with capacity to transport 1.34 Tcf (38 Bcm) per year across Eastern Russia to China. This spring, Gazprom began a feasibility study for the Power of Siberia-2, which could deliver another 1.77 Tcf/year across Mongolia to China.

In April, Gazprom approved a feasibility analysis of the proposed Soyuz Vostok gas trunkline. That pipeline would become an extension of the Power of Siberia 2 gas pipeline in Mongolian territory.

But Europe also remains squarely in its sights, and Gazprom announced in June that it had begun preparations to fill the first of the Nord Stream 2 twin pipelines with natural gas. It also said that only 62 miles (100 km) of pipeline was left to build, according to a TASS news agency report.

South & Central America

The midstream sector in South America was hit especially hard by low prices and weak demand brought on by Covid-19 shutdowns, with some companies cutting capital spending by a third, but there have been some glimmers of a rebound in recent months.

Colombia, for example, had to adjust its annual investment plan published in January 2020 to account for the economic decline, but its main national oil companies optimized resources to continue with plans for natural gas pipeline networks to help meet projected demand.

With Colombia’s Ministry of Mines and Energy projecting a national gas shortage by 2023-2025 due to the production declines in the Ballena and Cuisana regions, producers are looking to offset those losses by tapping their significant gas reserves in the Lower Magdalena area and delivering them to market via the $400 million Jobo-Transmetano pipeline.

The project is designed to interconnect with the National Transportation System at the Guacharacas Operating Station and scheduled to enter service in December 2024.

In Peru, Promigas subsidiary Gasnorp has signed a 32-year concession contract with Peruvian state for distribution of natural gas through a new pipeline network in the provinces of Piura, Talara, Sullana, Paita and Sechura.

The Argentine government, meanwhile, said it is implementing a $5.1 billion subsidy program to encourage domestic shale gas production in the Vaca Muerta formation. The program hopes to attract $5 billion in outside investment with planned infrastructure investments to include $600 million for the upgrade of two key Vaca Muerta pipelines.

South America in recent months has been a source of incremental demand for global LNG imports, fueled in part by low hydropower generation in Brazil, joining Asia Pacific in drawing LNG imports that would otherwise have gone to Western Europe.

Before the coronavirus outbreak, Brazil’s state energy research office said its growth projections justified construction of 16 new pipelines, but their future is uncertain after the country endured one the world’s most severe Covid-19 outbreaks.

Among the recommended pipelines, five would be offshore; among others, the largest would be a 563-mile (906-km) project connecting Sao Carlos to the capital city, Brasilia. Further east, the state of Bahia has already begun construction on the final section of the 190-mile, $100 million Southwest Gas pipeline.

Comments