May 2021, Vol. 248, No. 5

Features

Natural Gas Projects Boost Midstream in Early 2021

By Michael Reed, Editor-in-Chief

While no one can dispute that 2020 was not a good year for midstream, there has been some positive movement concerning natural gas pipelines – despite a year characterized by pricing woes and a crippling pandemic.

Toward the end of the year and into early 2021, about 4.4 Bcf/d (124 MMcm/d) of new natural gas pipeline capacity has entered service, according to data provided by the U.S. Energy Information Administration (EIA) for the period of November 2020 through January 2021.

Four projects added the bulk of that capacity:

- The Saginaw Trail Pipeline, a Consumer Energy interstate project replacing and expanding pipelines and other infrastructure, entered service in November 2020, with 200 MMcf/d (5.66 MMcm/d) of capacity in the central Michigan counties of Saginaw, Genesse and Oakland.

- The Buckeye Xpress, Columbia Gas Transmission’s (CGT) improvements project that replaced 66 miles (106 km) of 36-inch (914-mm) pipe in Ohio and West Virginia, added 300 MMcf/d (8.5 MMcm/d) of capacity from the Appalachia Basin into CGT’s interconnection in Leach, Ky., and the TCO Pool in West Virginia in December 2020.

- The Permian Highway Pipeline, a 430-mile (692-km) Kinder Morgan pipeline from the Waha Hub in West Texas, near production activities in the Permian Basin brought 2.1 Bcf/d (59 MMcm/d) of added capacity to Katy, Texas, near the Gulf Coast. It also has connections to Mexico.

- The Agua Blanca expansion, which went into service in late January, ships an additional 1.8 Bcf/d (51 MMcm/d) of natural gas to the Waha Hub. The Whitewater/MPLX connects to 20 processing sites in the Delaware Basin and connects with the 2-Bcf/d (57-MMcm/d) Whistler Pipeline, targeted for completion in the third quarter.

What would have been another large project, the 2-Bcf/d Permian Global Access Pipeline was canceled by Tellurian in December. It would have transported natural gas to a proposed liquified natural gas (LNG) facility in Gillis, La.

Midstream Overall

While demand has rebounded faster than expected in late 2020 and early 2021, optimism remains somewhat muted in the sector.

Nonetheless, analyses from the financial world have been surprisingly upbeat concerning midstream in recent months, especially in light of where we were just a few months ago.

Morgan Stanley upgraded its midstream outlook for 2021 outlook for midstream to “attractive for investors,” citing pipeline companies’ well-designed strategies for post-pandemic reopenings and “self-help” measures. “We see support for a sustained rally in midstream,” the analysis said.

So, the pipeline business in 2021 and beyond appears to be relatively stable, all things considered, and certainly in comparison to other energy sectors, such as exploration and production, which is affected more directly by volatility and oil and gas prices.

Early proof of this is that many midstream stocks returned to pre-COVID-19 levels in early March, led by such major players in North America as Williams, Kinder Morgan, Enbridge and TC Energy. In another promising sign, some smaller companies, such as Targa and Plains All American, did even better than the larger companies.

“A number of outside forces have certainly been working against us,” Maguire Energy Institute Executive Director Bruce Bullock recently told attendees of the Pipeline Opportunities Conference, citing zero-interest rates among those outside forces. “Every time the economy hiccups, the Fed turns around and lowers interest rates … it’s made money cheap and freely available.”

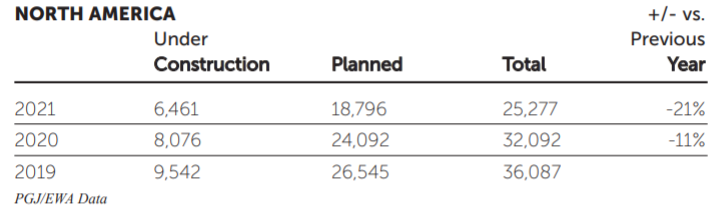

P&GJ data for last year showed a decline of 21% in miles of pipeline under construction, when compared to the previous year – from 32,092 miles (51,647 km) of planned and under construction pipeline at the end of 2019 to 25,277 miles (40,679 km) at the end of 2020. While there was also a decline in construction for the year ending 2019 vs. the year ending 2020, that decline was less – 11%.

Still, growth is expected to continue along the Gulf Coast for midstream, at least through 2025. This should increase investment, particularly when the COVID-19 adjustments taken by the sector are factored into consideration by investors.

This has prompted the Port of Corpus Christi in Texas to deepen part of its waterway, while two of its customers, Moda Midstream and Pin Oak, are planning significant oil storage capacity increases ahead of an anticipated jump in Chinese demand for US crude oil and LNG this year.

In North America, it comes as no surprise that the Permian remains the most active region. With EIA projecting shale oil production of nearly 4.24 MMbpd in December 2020, there is every indication 2021 production will increase.

The Permian should see significantly improved options with this eastbound expansion to the still burgeoning Texas Gulf Coast, where shipping at hubs remains reasonably attractive and should draw additional midstream projects.

Meanwhile, in the second-largest field in the United States, Bakken producers continue to face pressure to delay bringing back much of the 500,000 bpd of curbed crude output, following a court ruling in July that jeopardizes the operation of Energy Transfer’s Dakota Access Pipeline (DAPL), which ships most of the region’s oil.

An appeals court has allowed DAPL to continue operating for now, but the threat of closure makes reversing cutbacks and drilling new wells too risky, many executives and midstream analysts have said.

DAPL links Bakken producers to Midwest and Gulf of Mexico customers, accounting for about 40% of the volumes transported to those regions. Rail transport, which is $3 to $6 a barrel more expensive, is expected to expand if the pipeline should close.

Crude oil production in North Dakota is unlikely to bounce back to pre-COVID-19 levels until late 2022 due to reduced demand and pressure on investors from anti-fossil fuel forces.

In the midcontinent regions – the Marcellus and Utica – along with the SCOOP/STACK basin, companies will face difficulties beyond those brought on by fallout from the previous year.

Due, in part, to regulatory challenges to pipeline projects to the East Coast, and after already scaling back by about 20% in 2020, based on Gulf Energy Information’s Energy Web Atlas, much of the new year’s activity will likely focus on recovery efforts.

In what could turn out to be some good news for Marcellus-based companies, the U.S. Supreme Court agreed to hear an appeal by PennEast Pipeline Company to a ruling preventing it from seizing New Jersey state land.

Penn East would like to build a $1 billion, 120-mile (139-km) natural gas pipeline from Pennsylvania to New Jersey. Companies involved in the venture are Enbridge, South Jersey Industries, New Jersey Resources, Southern Co. and UGI.

Mountain Valley

A few, though certainly not all-inclusive, recent examples of cancellations and setbacks include the Northeast Supply Enhancement (NESE) project, postponed by Williams in May 2020 after a key permit was rejected, and delays to Mountain Valley Pipeline, which once again faces legal opposition in Virginia due to concerns about sedimentation and blasting that opponents say threaten endangered species.

Recently, Mountain Valley Pipeline said it plans to apply for individual stream-crossing permits instead of continuing to pursue a Nationwide Permit 12 from the U.S. Army Corps of Engineers. The company believes this is “the most efficient and effective path to project completion.” This new strategy should certainly be monitored closely by other midstream companies.

If all goes well, the Mountain Valley Pipeline will achieve its new targeted startup of 2022, the company said recently. However, in late March, Virginia’s Department of Environmental Quality told federal officials that it will not be able to issue a new water quality permit for the project’s stream crossings before December.

New Administration

Along with more onerous regulations to sift through, there likely will be further consolidation between larger diversified companies and smaller midstream operations for companies to navigate.

These diversifications are in outright sales, such those occurring last year: the Devon Energy acquisition of Permian Basin peer WPX Energy for $2.56 billion and CenterPoint Energy’s sale of Miller Pipeline and Minnesota Limited to PowerTeam Services for $850 million.

More mergers such as the Husky Energy-Cenovus agreement that resulted in the creation of Canada’s No. 3 oil and gas producer are bound to occur, as well.

On the political front, during the U.S. presidential campaign, then-candidate Biden announced an ambitious $2 trillion “clean energy revolution” to accelerate the U.S. energy transition to renewables, including setting a net-zero carbon emission target in the power sector by 2035. Biden also said he would initiate the United States’ return to the Paris Climate Agreement, which is already underway.

If implemented, some of Biden’s policies could have long-term effects on the U.S. energy landscape. Although the policies are beyond executive orders, the slim majority held by Democrats would likely slow much of the “net-zero” push in Congress.

More Recent Developments

- On an upbeat note for New England, early in the year, Enbridge’s Atlantic Bridge project was placed into full service in January, following completion of the Weymouth Compressor Station, which facilitates delivery of much-needed natural gas to project customers in Maine and Atlantic Canada.

- Midcoast Energy, through an East Texas operating subsidiary, has entered into a commercial agreement with an anchor shipper to support the expansion of its pipeline system to provide transportation of natural gas supplies from East Texas to the Texas Gulf Coast (CJ Express). The CJ Express expansion project is expected to be in service in early 2021.

- S. regulators approved construction work on almost all of the 135-mile (218-km) Summit Double E Pipeline, linking natural gas production areas in the Permian’s Delaware Basin to the Waha Hub in Texas. The 1.35-Bcf/d (39-MMcm/d) pipeline will interconnect the Gulf Coast Express and the Permian Highway pipelines, and the Trans-Pecos pipeline. The Double E is expected online in the fourth quarter of 2021.

Comments