April 2022, Vol. 249, No. 4

Features

Short-Term Energy Outlook Heavily Influenced by Russia’s Invasion

By Energy Information Administration (EIA)

EIA’s March Short-Term Energy Outlook (STEO) addresses heightened levels of uncertainty resulting from a variety of factors, including Russia’s further invasion of Ukraine.

The STEO assumes U.S. gross domestic product (GDP) will grow by 3.6% in 2022 and by 2.7% in 2023, after growing by 5.7% in 2021.

Global macroeconomic assumptions in our forecast are from Oxford Economics and include global GDP growth of 4.3% in 2022 and 4.0% in 2023, compared with growth of 5.9% in 2021. These GDP forecasts were completed in mid-February. The rest of the forecast was completed on March 3 and accounts for available information to that point.

A wide range of potential macroeconomic outcomes could significantly affect energy markets during the forecast period — supply uncertainty results from the conflict in Ukraine, the production decisions of OPEC+ and the rate at which U.S. oil and natural gas producers increase drilling.

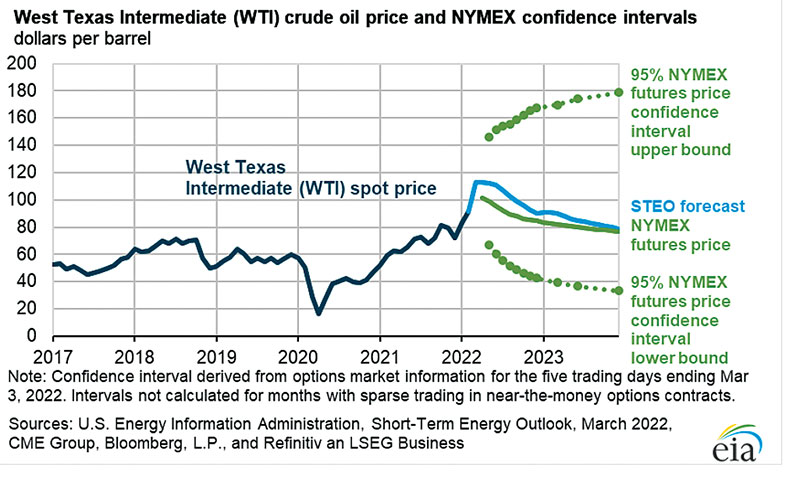

Brent crude oil spot prices averaged $97 per bbl in February, an $11 per bbl increase from January. Daily spot prices for Brent closed at almost $124 per bbl in the first week of March as the further invasion of Ukraine by Russia and subsequent sanctions on Russia and other actions created significant market uncertainties about the potential for oil supply disruptions.

These events are occurring against a backdrop of low oil inventories and persistent upward oil price pressures. Global oil inventories have fallen steadily since mid-2020, and inventory draws averaged 1.8 MMbpd from the third quarter of 2020 through the end of 2021.

EIA estimates oil inventories fell further in the first two months of 2022 and that commercial inventories in the OECD (Organisation for Economic Co-operation and Development) ended February at 2.64 billion bbl, which is the lowest level since mid-2014.

Brent price is expected to average $117 per bbl in March, $116 per bbl in second-quarter 2022 and $102 bbl in the second half of 2022. Average prices are expected to fall to $89 per bbl in 2023.

However, this price forecast is highly uncertain. Actual price outcomes will be dependent on the degree to which existing sanctions imposed on Russia, any potential future sanctions and independent corporate actions affect Russia’s oil production or the sale of Russia’s oil in the global market. In addition, the degree to which other oil producers respond to current oil prices, as well as the effects macroeconomic developments might have on global oil demand, will be important for oil price formation in the coming months.

Although reduced Russian oil production is forecast, global oil inventories are expected to build at an average rate of 500,000 bpd from the second quarter through the end of 2023. This will likely put downward pressure on crude oil prices. However, if production disruptions – in Russia or elsewhere – are more than forecast, resulting crude oil prices would be higher than our forecast.

EIA forecasts that global consumption of petroleum and liquid fuels will average 100.6 MMbpd for all of 2022, up 3.1 million bpd from 2021. EIA foresees consumption increasing by 1.9 MMbpd in 2023 to average 102.6 MMbpd.

Economic forecasts in this outlook were completed before Russia’s further invasion of Ukraine. The outlook for economic growth and oil consumption in Russia and surrounding countries is highly uncertain. Oil consumption will depend on how economic activity and travel respond to recent and any potential future events and sanctions.

U.S. crude oil production fell below 11.6 MMbpd in December 2021 (the most recent monthly historical data point), a decline of 200,000 bpd from November 2021. EIA forecasts that production will rise to average 12 MMbpd in 2022 and then to record-high production on an annual average basis of 13 MMbpd in 2023. The previous annual average record of 12.3 MMbpd was set in 2019.

Natural Gas

In February, the Henry Hub natural gas spot price averaged $4.69 per million British thermal units (MMBtu), which was up from the January average of $4.38/MMBtu. Although temperatures across the eastern part of the United States were close to normal in February, reducing natural gas consumption from January levels, natural gas production fell slightly last month relative to January, in part as a result of temporary freeze-offs in producing regions. The drop in production partly contributed to inventory draws outpacing the five-year (2017–2021) average in February.

This outlook assumes that temperatures in March will be milder than February and near the 10-year average for March. EIA expects production will rise from February levels, contributing to a lower average Henry Hub price of $4.10/MMBtu for March. EIA expects the Henry Hub price will average $3.83/MMBtu in second-quarter 2022 and $3.95/MMBtu for all of 2022. The Henry Hub spot price is expected to average $3.59/MMBtu in 2023.

EIA estimates that inventory withdrawals in February were 627 Bcf (18 Bcm) and that natural gas inventories ended the month at 1.6 Tcf (45 Bcm). EIA expects natural gas inventories to fall by about 95 Bcf (2.7 Bcm) in March, ending the withdrawal season at about 1.5 Tcf (42 Bcm), which would be 10% less than the five-year average for this time of year. Natural gas inventories are expected to end the 2022 injection season (end of October) at 3.5 Tcf (99 Bcm), which would be 4% less than the five-year average.

In February, U.S. liquified natural gas (LNG) exports averaged 10.9 Bcf/d (309 MMcm/d), down from 11.2 Bcf/d (317 MMcm/d) in January. Similar to last year, U.S. LNG exports in February were limited by fog in the Gulf of Mexico, which affected vessel traffic and led to piloting services being suspended for several days on the Sabine Pass, Lake Charles (location of Cameron LNG), and Corpus Christi waterways.

Although exports fell in February, they were higher than in any month prior to December 2021. Many U.S. LNG cargoes were delivered to Europe last month, where inventories are lower than the five-year average, and potential supply disruptions related to the conflict in Ukraine are a concern.

Although Europe’s inventories are low, the additional LNG imports, as well as a mild winter, are helping bring inventories closer to the five-year average than they were at the beginning of the winter. EIA expects high levels of U.S. LNG exports to continue in 2022, averaging 11.3 Bcf/d (320 MMcm/d) for the year, a 16% increase from 2021.

EIA expects U.S. consumption of natural gas will average 84.6 Bcf/d (2.4 Bcm/d) in 2022, up 2% from 2021. The increase in U.S. natural gas consumption reflects rising demand in the industrial sector as a result of increased manufacturing activity. In addition, the increase in natural gas consumption reflects higher consumption in the residential and commercial sectors as a result of colder temperatures this year compared with 2021.

Lower consumption in the electric power sector partly offsets higher consumption in these sectors due to a forecast increase in generation from renewable energy sources.

EIA estimates dry natural gas production averaged 95.3 Bcf/d (2.70 Bcm/d) in the United States in February, down 0.6 Bcf/d from January. Production in January and February was lower than in December because of freezing temperatures in certain production regions.

Natural gas production is projected to average 95.7 Bcf/d (2.7 Bcm/d) in March. For 2022, EIA expects natural gas production will average 96.7 Bcf/d (2.74 Bcm/d), which is 3.1 Bcf/d (88 MMcm/d) more than in 2021. EIA expects dry natural gas production to rise to an average of 99.1 Bcf/d (2.8 Bcm/d) in 2023.

Comments