December 2013, Vol. 240 No. 12

Features

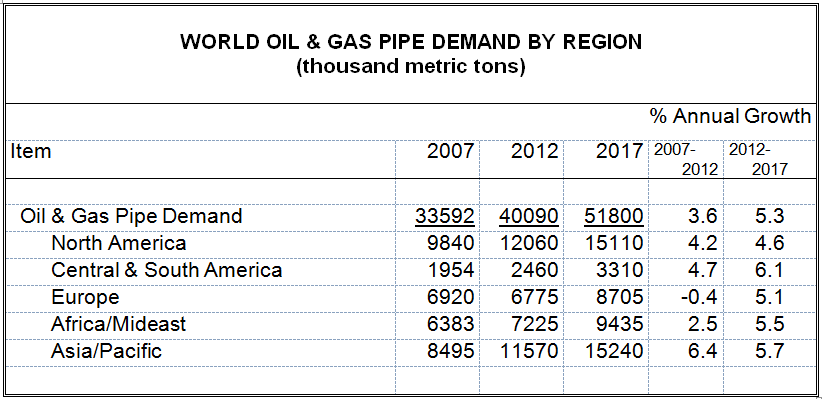

World Oil And Gas Pipe Demand To Reach 51.8 Million Metric Tons In 2017

World demand for oil and gas pipe is expected to increase 5.3% per year, reaching 51.8 million metric tons in 2017 as high oil prices and increasing demand for energy spur new development.

Increased oil and gas production will require additional investment in pipeline infrastructure. Demand for gas pipe will strongly outpace that for oil pipe, due in large part to infrastructure development. New pipelines will range from domestic lines to transnational systems that deliver natural gas to markets such as Europe. These and other trends are presented in World Oil & Gas Pipe, a new study from The Freedonia Group, Inc., a Cleveland-based industry market research firm.

Demand gains for oil country tubular goods (OCTG) will outpace growth in the number of drilling rigs through the forecast period, due in part to rigs becoming more efficient and drilling more wells per year. In addition, rising OCTG pipe demand will result from increased offshore activity, deeper wells and growing use of horizontal drilling techniques. Each of these techniques requires the use of more pipe than traditional onshore wells. Higher pressure drilling techniques require increased pipe wall thicknesses which will increase the tonnage of OCTG pipe.

Seamless steel pipe will remain the dominant product in this application due to strength in these harsh environments. Development of improved premium connections better suited to cope with harsh operating conditions will create opportunities in the OCTG market, since users are willing to pay more to ensure proper operation.

Demand for line pipe will benefit from construction of new transmission lines needed to transport oil and gas from drilling sites to customers, and the need for gathering systems at new drilling sites.

Plastic pipe demand will grow as it gains share from steel in gathering applications. Steel pipe will remain the dominant line pipe material because of its high pressure resistance. Seamless pipe has outpaced welded pipe in recent years, reflecting strong growth for OCTG since those applications more frequently require the strength of seamless pipe.

Due to its lower price, welded pipe will continue to be preferred in applications where operating conditions allow its use. Demand for distribution pipe will benefit from rising residential construction expenditures, which will boost the need for natural gas lines to new homes.

North America is by far the largest regional market for oil and gas pipe, accounting for 30% of total demand in 2012. The U.S. alone accounted for nearly 24% of global demand in that year, and both Canada and Mexico are among the top 15 national markets. This is due to the large number of producing wells, well completions, and drilling rigs needed to maintain production from North America’s mostly mature oil and gas fields. There is generally far less drilling activity in Mexico than in the U.S. or Canada, but Mexico is a notable outlet for pipe due to its significant energy output and offshore activity.

Oil and gas pipe demand in the Asia/Pacific region – the second largest regional market – is expected to register above average growth. Future gains will be driven by the expansion of the offshore sector, including in the Caspian Sea and a number of spots in the Pacific Ocean, which will lead to greater use of pipe per well drilled.

Growth in oil and gas drilling activity is expected to fuel gains for oil and gas pipe in Central and South America. Brazil and a number of other countries in the region are expanding both their drilling activity and their oil and gas output, providing strong growth opportunities through the forecast period, although the regional market will remain comparatively small. Much of the new development will be in deep offshore areas off the coast of Brazil, which will benefit pipe demand since some of these wells are over 4,000 meters deep.

Oil and gas production in the Africa/Mideast region has historically been less pipe-intensive than in other regions due to the relative ease of hydrocarbon extraction in much of the region, particularly in the Middle East. Wells there have been relatively shallow and have not needed pipe-intensive techniques, such as horizontal drilling. However, expanding exploratory and developmental activity, particularly in offshore areas (such as off Africa’s west coast), will support increases in pipe usage.

Additionally, growth in oil and gas production in the region will be well above the global average. Future gains will be further supported by efforts to develop the region’s extensive natural gas resources beyond current associated output, and to maintain production as the world’s most productive oilfields mature. Natural gas production in the region is expected to grow much faster than the global average, as many countries in the region will try to use natural gas for an increasing share of their domestic energy needs, often to make more crude oil available for export.

Natural gas pipe will post stronger gains than oil pipe through the forecast period. Most of the major pipeline projects planned worldwide involve transport of natural gas. For example, China broke ground on its 7,300 km West-East Pipeline III in October 2012. In addition, drilling activity for natural gas will pick up as demand increases. In addition, demand for pipe in the oil market will benefit from increased offshore drilling.

Steel is by far the dominant oil and gas pipe material. Welded pipe, particularly electric resistance welded (ERW) and longitudinal submerged arc welded (LSAW), will narrowly retain the largest portion of steel pipe demand through 2017. Plastic pipe will continue to see a rising share of smaller diameter applications such as gathering pipe, but will account for less than 10% of the market through 2017 and beyond.

World Oil & Gas Pipe (published October 2013, 347 pages) is available for $6100 from The Freedonia Group, Inc., 767 Beta Drive, Cleveland, OH 44143-2326. For details, contact Corinne Gangloff by phone 440.684.9600, fax 440.646.0484 or e-mail pr@freedoniagroup.com.

Author:

Michael Deneen has been an industry analyst with The Freedonia Group since 1998, writing such titles as World Pumps, World Water Pipe, World Valves, Oil & Gas Infrastructure, and World Water Infrastructure Equipment. He has a bachelor’s degree from Northwestern University and a master’s degree from Cleveland State University. Previous to joining Freedonia, he was employed by State Chemical Manufacturing Co.

Comments