September 2018, Vol. 245, No. 9

Features

Strategy Shaped by Volatility

By Reid Morrison, Principal, PwC US

After several years of oversupply, the oil and gas industry could be headed into a supply crunch. This may seem difficult to imagine. According to the U.S. Energy Information Administration (EIA), oil prices have almost doubled in the past two years – from $38.84 per barrel in January 2016 to $72.35 per barrel in May 2018.

Although the industry feels much healthier than it did 12 months ago, during the downturn companies reacted by focusing primarily on production and cutting costs. However, oil demand is growing, and the public’s assumption is that supply is easy to access. Because major projects were deferred during the downturn, the reality is there is less available supply to quickly bring to market. This means oil companies will need to resume exploration and development in an environment in which capital investment is based on returns. This could be a struggle for some companies.

In the short term, businesses must enforce capital discipline, focus on productivity improvements and apply new technology. Looking long term, companies will need to deliver a positive return on capital and maintain a free cash flow disciplined mentality to ensure a profitable enterprise.

Major Supply Challenges

Oil and gas rig activity levels are rising and being driven by the North American market, and with exploration on the rise again for the first time since the global recession, numerous companies are getting back to the hard work of finding and developing reserves.

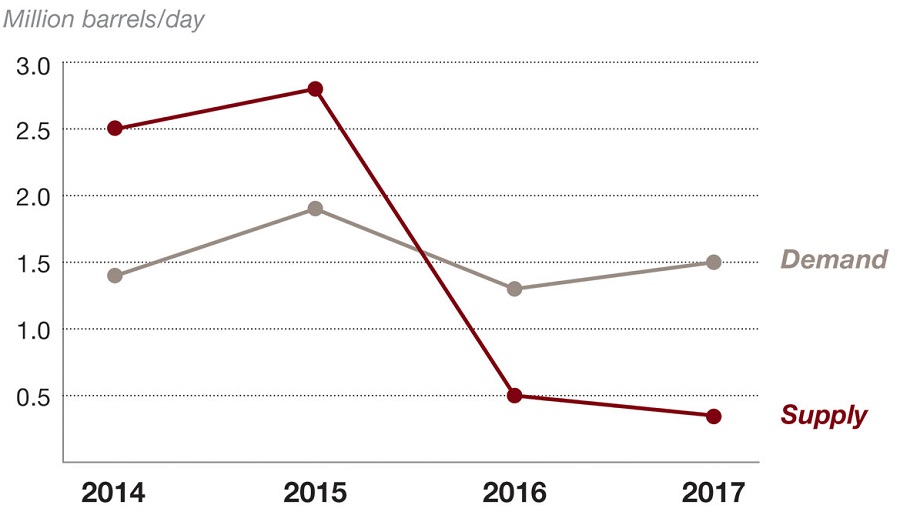

Despite these positive signals, there are five major supply-related challenges the industry faces. First is the ongoing low rate of new discoveries due to limited capital, which limits finding large discoveries and constrains greenfield exploration. To put this in perspective, only 3.5 billion barrels of liquids were discovered in 2017, according to EIA, which was enough to meet only 10% of the demand.

The second challenge affecting supply is the slow speed of the rise in exploration spending. These first two challenges combined have created what the IEA is calling a “two-speed oil market,” which is the result of declining investment in conventional sources and preference for investments in unconventional plays.

The decline in investment during the downturn could continue to hurt the industry, if it remains constrained, especially given the additional 3 MMbpd of new production needed each year just for conventional output to remain flat, coupled with the fact that offshore projects take about four to six years to come online.

Thirdly, supply disruption continues to challenge the industry beyond the production decline rates. Disruption around the globe is due in part to geopolitical issues, which periodically challenge OPEC’s production levels and spare capacity.

Fourthly, deferred maintenance continues to challenge global production as operators deferred noncritical spending to reduce costs. Although important everywhere, maintenance is critical in basins with aging asset infrastructure, as recently evidenced by the crack in the North Sea Forties pipeline, which disrupted production in the region and highlighted the challenges for an asset that is more than 15 years past its original design life of 25.

The fifth challenge relates to the changing workforce. Workforce reductions made during the downturn resulted in damages to both technical skills and the industry’s ability to attract new talent.

These five challenges mean that U.S. tight oil operators are under mounting pressure from investors to shift from an all-out production growth model to more profitable operations, and development of conventional and offshore production remains cautious as confidence is rebuilt the necessary capital will generate a satisfactory return.

‘Future-Proof’

Regardless of the short-term volatility, businesses must embrace “future-proofing” strategic principles to overcome the uncertainties of a potential supply crunch and the energy needs of the future. Companies of all sizes, including smaller independents, must continue to manage and review the overall portfolio with a much lower break-even price and eliminate assets that don’t fit.

Using the mantra of capital discipline, companies need to ensure that all operational decisions reflect the company’s core and differentiated capabilities, so that inefficiencies do not creep in. A high level of free cash will be critical for oil and gas companies, which means living within existing cash flow is the new reality. Since success in the market correlates with financial returns as opposed to production volume, the entire company will benefit.

As oil prices rise, there is temptation to push production equipment harder to produce more. Operators must first ensure adequate funds to keep infrastructure in good condition – especially if maintenance was deferred in recent years.

A best practice that many oil exploration and production companies should implement would be to shift away from the “owner-operator” model in which capabilities are built across the entire value chain, as the costs incurred under this construct outweigh the value generated. Companies should seek out partnerships with other best-in-class companies to form an ecosystem of expertise. This means new operating models that assemble expertise across the value chain, replace fixed costs with variable costs, and set up commercial terms that balance risk, reward and roles.

As technology advances, oil and gas companies need to drive innovation across their businesses. Leveraging digital technology to improve efficiency can open new opportunities, processes and practices. This can take the form of using drones to inspect offshore platforms, which reduces workers’ exposure to hazardous tasks or data analytics to optimize production. There will be a new demand for expertise in digital operations that must be weighed against traditional disciplines such as subsurface and surface engineering.

In the longer term, companies must focus on finding and executing the most resilient future-proof strategy for their own unique capabilities. This could take the form of entry into new types of energy operations, divestiture of existing assets, investments in lower-carbon plays and shifting toward natural gas.

Conclusion

Many people are overconfidence about supply, neglecting the supply side of the global energy situation. As demand continues to exceed annual forecasts, volatility is also likely to affect oil prices. As operators assess the impact of various scenarios from supply constraints, a plan of action will be needed.

In the near term, portfolios have to be resilient, innovation needs to thrive, and capital efficiency must remain the bedrock of operations. Longer term, companies will need a robust strategy to deliver free cash flow from hydrocarbons: a strategy that will serve them no matter what the future brings. Only the companies that can do all this will prevail. P&GJ

Author: Reid Morrison leads PwC’s global energy advisory practice. Based in Houston, he is a principal with PwC US. He has more than 24 years of experience in the oil and gas industry. He advises clients on strategies and initiatives to improve operational and commercial performances.

Comments