September 2019, Vol. 246, No. 9

Features

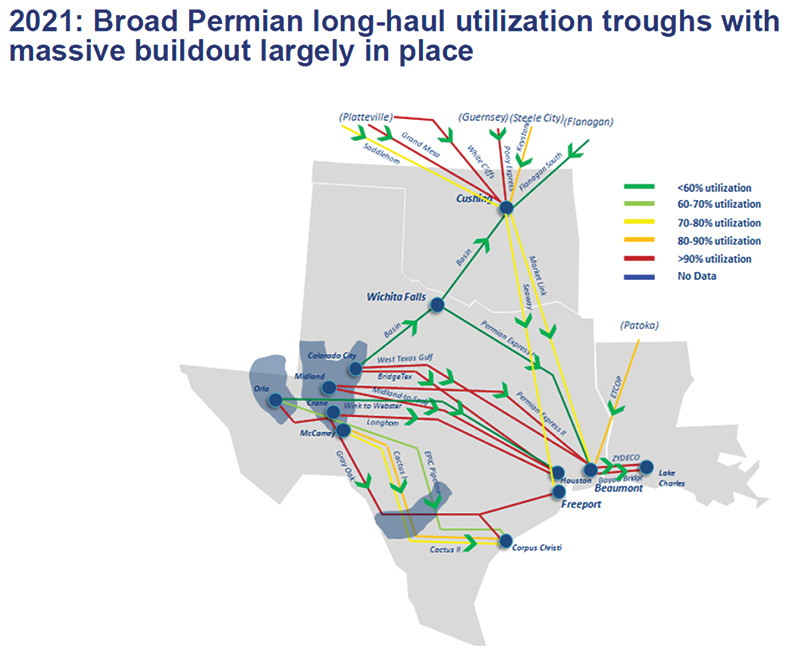

New Pipelines Open Permian Tap as Demand Outlook Grows Cloudy

By Jeff Awalt, Executive Editor

After scrambling to catch up with fast-growing Permian Basin crude oil production, pipeline operators appear to be entering a period of excess takeaway capacity with the completion of new and expanded systems this year.

This “over-piped” period is expected to be fairly short-lived, however, as Permian crude oil production is projected to grow significantly in coming years, despite investor pressure on shale producers, a shortage of export infrastructure and signs that global demand may be cooling amid trade disputes.

Construction between the Permian Basin and the Gulf Coast, meanwhile, will remain brisk with natural gas pipeline projects at least through 2021, along with the continuing development of storage and export infrastructure for crude oil and LNG.

Crude Oil

Shale advancements and the removal of a U.S. ban on oil exports in December 2015 combined to create a perfect storm for Permian Basin expansion. Average daily production is growing at a rate of roughly 1 million barrels per year – from 3.2 MMbpd in 2018 to 4.2 MMbpd in April 2019, when the Permian officially became the world’s most prolific field. It’s about 4.42 million today.

Pipeline operators answered the growing oil production with a half-dozen major construction or expansion projects, starting with Enterprise Products’ well-timed 575,000-bpd Midland-to-Sealy pipeline. Commencing limited commercial operations in late 2017, it commanded a 25% tariff premium as oil production in the Permian neared pipeline takeaway capacity. Crude oil capacity additions since then include:

- Plains All American completed its 500,000-bpd Sunrise Pipeline expansion in October 2018.

- Enterprise Products added 200,000 bpd of capacity from the Permian Basin to Houston with the conversion of its Seminole-Red NGL pipeline to crude oil in early 2019.

- Energy Transfer Partners’ Permian Express 4 expansion was scheduled to add 120,000 bpd when it begins service by the end of this month.

The startup of three more major crude oil pipelines in 2019 will add 2.5 MMbpd of capacity from the Permian Basin to Corpus Christi:

- Plains All American commenced shipments of crude oil for Trafigura Trading via the Cactus II Pipeline in early August, marking the first confirmed shipments on Plains’ newly operational system. The line was expected to flow about 300,000 bpd during its first month of operation and be near capacity in September.

- Epic Midstream Holdings last month began filling its 900,000 bpd EPIC Crude pipeline originating in Orla, Texas. The system includes eight terminals and will serve the Delaware, Midland and Eagle Ford basins.

- The 850-mile Gray Oak Pipeline, also with a capacity of 900,000 bpd, is scheduled to begin operations later in 2019. It will also connect to market centers in Sweeny and Freeport, Texas.

In a clear sign that takeaway capacity is catching up with near-term demand, operators of the new pipelines have been offering discounted spot prices to attract shippers.

Shrinking pipeline capacity in late 2017 enabled Enterprise Products to set a tariff of $6.74 a barrel as its Midland-to-Sealy came into service, compared with next-highest Plains Cactus I at $4.24 and Magellan Longhorn at $4.15.

With significant new capacity coming online in 2019, Plains set contract rates between $1.05 and $3.20 a barrel and spot rates of $4.75 to $5.60 a barrel for Cactus II, according to federal filings, with most of its capacity believed to be under contract. Likewise, EPIC halved the spot rate to $2.50 a barrel on its new crude oil pipeline from the Permian before it began loading the 400,000-bpd line, describing the new rate as being “more in line with market conditions.”

In addition to the 2.4 Bcfd of capacity starting service in 2019, there are at least three more Permian crude oil pipelines planned for completion during the next two years:

Red Oak Pipeline – Plains All American and Phillips 66 announced in June that they sanctioned construction of the new joint-venture Red Oak Pipeline to transport oil from the Permian Basin and Cushing, Okla., upon its planned completion in 2021. Red Oak, which will lease capacity in Plains’ Sunrise system, is designed to transport 400,000 bpd to Houston and multiple locations along the Texas Gulf Coast.

Jupiter Pipeline – Jupiter Energy said it has secured funding for its planned 650-mile, 36-inch crude oil pipeline from the Permian to the Brownsville (Texas) Terminal for completion in 2020. In Brownsville, Jupiter said it is adding up to 10 million barrels of storage, along with three docks in the Port of Brownsville and an offshore very large crude carrier (VLCC) loading facility.

Wink to Webster Pipeline – The Wink-to-Webster Pipeline will provide more than 1 MMbpd of crude oil and condensate capacity upon its expected completion by early 2021. The project is a joint venture among affiliates of ExxonMobil, Plains All American, Lotus Midstream, MPLX, Delek US and Rattler Midstream. The project is underpinned by a significant volume of long-term commitments.

Natural Gas

Fast-rising oil production in the Permian Basin has led to soaring levels of associated gas production, resulting in pipeline bottlenecks, severely depressed prices and record levels of gas flaring by oil producers.

By early of this year, production had so overwhelmed natural gas takeaway capacity that prices began trading in negative territory, upending producer economics. Apache Corporation, notably, announced a temporary halt in production at its Alpine High assets in April, curtailing output of about 250 MMcf of natural gas.

Those constraints will begin easing as four significant natural gas pipeline projects come online through 2023, and Kinder Morgan – the developer of two of those projects – is evaluating demand for yet another for potential completion in 2022.

Gulf Coast Express (GCX) – Kinder Morgan started construction on the $1.75 billion GCX project in May 2018. Designed to transport up to 2 Bcf/d of natural gas from the Permian Basin to the Agua Dulce, Texas, area, it is now fully subscribed under long-term, binding transportation agreements. GCX remains on schedule for a full in-service date of October 2019.

Permian Highway Pipeline (PHP) – The 430-mile, 2-Bcf/d PHP, a joint venture of Kinder Morgan and EagleClaw Midstream Ventures, is scheduled to come online in 2020 to deliver Permian gas nearer the center of Kinder Morgan’s system and meet LNG and industrial demand in the Freeport area.

Whistler Pipeline – Whistler is designed to transport 2 Bcf/d of natural gas through 475 miles of 42-inch pipeline from Waha to Agua Dulce beginning in 2021. It will source gas from multiple Permian connections, including direct connections to plants in the Midland Basin through a 50-mile, 30-inch lateral and a direct connection to the 1.4 Bcf/d Agua Blanca Pipeline. A final investment decision on Whistler was reached in 2018 by project partners MPLX LP, WhiteWater Midstream, and a joint venture between Stonepeak Infrastructure Partners and West Texas Gas, Inc.

Permian Pass Pipeline (PPP) – Kinder Morgan is in the early stages of evaluating potential development of Permian Pass, which could begin delivering 2 Bcf/d of natural gas from West Texas to the Sabine area of the East Texas-Louisiana Gulf Coast as early as 2022. By transporting gas to East Texas to serve LNG demand around Sabine, Permian Pass would complement Kinder Morgan’s GCX and PHP projects, said CEO Steven Kean, who noted that 70% of natural gas demand growth through 2030 is expected to be in Louisiana and Texas.

Permian Global Access Pipeline (PGAP) – An open season in May for PGAP drew strong demand from Permian producers seeking delivery to the rapidly growing natural gas market in Southeast Louisiana, and Tellurian is working with prospective shippers on agreements. The $3.7 billion PGAP is a proposed 625-mile, 42-inch gas pipeline originating at the Waha Hub and terminating at Gillis, La., north of Lake Charles. Construction of the 2-Bcf/d line could begin as early as 2021, with service beginning by 2023.

PGAP is one of three proposed pipelines that would comprise the estimated $7.3 billion Tellurian Pipeline Network, which is integral to its planned $15.2 billion Driftwood LNG export project near Lake Charles.

Export Infrastructure

As pipeline constraints ease, new bottlenecks may occur if Permian crude oil volumes to the Texas Gulf Coast outpace the construction of expanded export infrastructure. There also is a likelihood of traffic congestion due to the Corpus Christi channel’s inability to handle VLCC tankers, requiring use of smaller tankers for ship-to-ship transfers in deeper waters until more VLCC terminals come online.

The three new crude oil pipelines starting service from the Permian this year will have the capacity to deliver up to 2.5 MMbpd of crude oil to Corpus Christi, where six export terminals are slated for construction through 2023.

- The first of these – the 960,000-bpd Eagle Ford Terminal – is a joint venture of Enterprise Products and Plains All American scheduled for completion this year.

- Two terminals scheduled for completion in 2020 include the EPIC/CCI South Texas Terminal with a load rate of 154,000 bpd and the 800,000-bpd South Texas Gateway/Ingleside developed by Buckeye, Phillips 66 and MPLX.

- The remaining planned VLCC-capable terminals are all targeting completion in 2023. They include the Port of Corpus Christi/Carlyle 1.4-MMbpd Harbor Island project, Trafigura’s 500,000-bpd Texas Gulf Terminal and Phillips 66’s proposed 1.9-MMbpd Bluewater Texas Terminal.

Forecast

Despite growing concern over a flight of capital from Permian independents and doomsday speculation that the “shale boom” may be coming to an end, the outlook for Permian Basin exploration and production, midstream services and pipeline construction remains positive overall.

The U.S. Energy Information Administration (EIA) projects continuing record crude oil production from the Permian Basin, and even those voicing concerns about declining shale output growth tend to separate the Permian from other basins. Pioneer Natural Resources CEO Scott Sheffield, for instance, warned recently the shale boom could end by 2025, but added that the Permian’s Midland Basin should continue to expand output beyond that year.

“We are in the midst of one of the largest crude infrastructure investment booms in U.S. history, with much of the investment focused on the Permian basin,” said John Coleman, Wood Mackenzie’s principal analyst for North America crude markets.

“As massive as this current investment wave is, we don’t think the story is yet finished,” he added. “More capacity additions will be needed again by the end of the next decade.”

The latest Wood Mackenzie North America Crude Markets Service long-term outlook shows that even with the rapid buildout in the early 2020s, there will be one more call for additional Permian-to-Gulf Coast pipeline capacity. The analysis indicates at least 300,000-500,000 bpd of crude takeaway capacity will be needed. Based on forecast market demand, an FID on the next needed pipeline may come in the late 2020s, WoodMac said.

The greatest risk is pricing, and Morningstar Research Director Sandy Fielden pegs $55 as the key number for the Permian.

“If prices stay above $55/barrel, production will continue to grow in sweet spots like the Permian Basin,” Fielden said, with majors like Chevron and ExxonMobil continuing to produce, even if independents are squeezed by financial constraints.

On the other hand, if prices drop below $55 for a sustained period, “then the current production stall could turn into a bust,” Fielden said, and “as soon as production starts to fall, exports will follow suit.” P&GJ

Comments