May 2022, Vol. 249, No. 5

Features

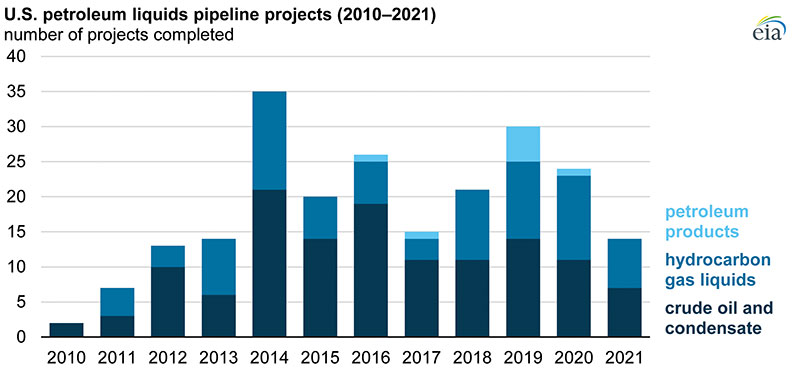

EIA Update: Last Year, 14 Liquids Pipeline Projects Completed In US

By U.S. Energy Information Administration (EIA)

In 2021, pipeline companies completed 14 petroleum liquids pipeline projects in the United States, according to the U.S. Energy Information Administration’s (EIA’s) updated Liquids Pipeline Projects Database.

This total consists of seven crude oil pipeline projects and seven hydrocarbon gas liquids pipeline projects. No petroleum product pipeline projects were completed last year.

Of the 14 completed projects:

- Six projects were new pipelines.

- Five projects were expansions of existing systems.

- Two projects reversed the direction of the flow on the pipeline.

- One project was a change in the commodity carried by the pipeline.

During 2021, 11 projects were announced, and two projects were listed by companies as under construction. An additional 10 projects were permanently canceled, and five projects were put on temporary hold as of the end of 2021.

Notable completions in 2021

Enbridge – Line 3 and Line 61 are two expansion projects that transport crude oil from Alberta, Canada, to Illinois. Line 3 goes from Alberta to Superior, Wisconsin. Line 61 goes from Superior to Pontiac, Illinois.

Marathon Pipe Line – The Capline Reversal project reversed the direction of the pipeline to a south-flowing pipeline that originates in Patoka, Illinois, and flows down to various terminals in St. James, Louisiana.

Energy Transfer – The Dakota Access Pipeline (DAPL) Expansion project increased capacity by 180,000 bpd along the DAPL system by adding horsepower and a few modifications and upgrades at pump stations. The DAPL system runs from North Dakota, through South Dakota and Iowa, and ends near Patoka, Illinois.

The compiled information considers more than 250 future, ongoing and past liquids pipeline projects in the United States. These pipelines carry crude oil, hydrocarbon gas liquids, and petroleum products, which include gasoline, diesel, jet fuel and other refinery products, and dates to 2010.

Some projects are related to each other and may carry the same fuels to their final destination. As a result, adding together the capacity of all projects would result in overestimating or double counting some pipeline capacity.

EIA data reflect reported plans and do not reflect assumptions on the likelihood or timing of project completion.

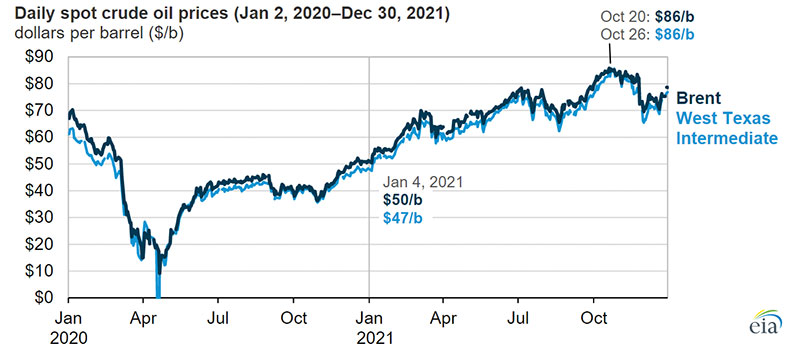

Crude Oil Prices Increased as Global Demand Outpaced Supply

Crude oil prices increased in 2021 as increasing COVID-19 vaccination rates, loosening pandemic-related restrictions and a growing economy resulted in global petroleum demand rising faster than petroleum supply.

The spot price of Brent crude oil, a global benchmark, started the year at $50 per barrel and increased to a high of $86 per barrel in late October before declining in the final weeks of the year.

Brent’s 2021 annual average of $71 per barrel is the highest in the past three years. The price of West Texas Intermediate (WTI) crude oil traced a similar pattern to Brent and averaged $3 a barrel less than Brent in 2021.

Global petroleum production increased more slowly than demand, driving higher prices. The slower increase in production was mostly attributable to OPEC+ crude oil production cuts that started in late 2020.

OPEC and other countries, such as Russia, which coordinate production with OPEC (referred to as OPEC+), announced in December 2020 that they would continue to limit production increases throughout 2021 to support higher crude oil prices.

According to the December 2021 Short-Term Energy Outlook (STEO) estimates, U.S. crude oil production in 2021 decreased by 0.1 bpd from 2020 and by 1.1 MMbpd from 2019. Cold weather in February and hurricanes in August contributed to this decrease, but it also was a result of the decline in investment among U.S. oil producers since mid-2020.

Increasing demand and a lower supply of crude oil resulted in consistent global petroleum and liquid fuels inventory withdrawals from February through December and contributed to increasing crude oil prices.

The largest inventory draw was in February, when Saudi Arabia imposed a cut of 1 MMbpd on its production, and the United States experienced extremely cold weather that led to well freeze-offs and a 1.3-MMbpd decline in crude oil production.

Withdrawals were also high in June, one month before OPEC+ announced it would begin increasing crude oil production each month. In the December 2021 STEO, it was estimated that petroleum inventories decreased by 469 million barrels globally in 2021 – likely the largest annual inventory withdrawal since 2007.

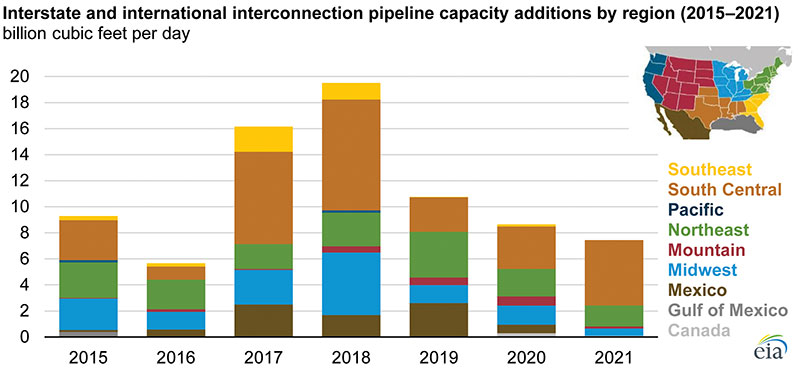

Interstate Gas Pipeline Capacity Additions Decrease in 2021

A total of 7.44 Bcf/d (211 MMcm/d) of interstate natural gas pipeline capacity was added in the United States during 2021, according to our recently updated Natural Gas Pipeline Projects Tracker. This amount was the lowest amount of capacity added to interstate transmission since 2016.

Interstate pipelines are those that cross state borders and that serve export demand, both at pipeline border crossings and at terminals exporting liquefied natural gas (LNG). The Federal Energy Regulatory Commission (FERC) regulates these pipelines.

More than two-thirds of the new interstate natural gas pipeline capacity, or 5.01 Bcf/d (142 MMcm/d), was added to transport natural gas into and within Texas and the Gulf Coast markets, which we define as the South-Central region. Most of the additional capacity is intended to serve growing LNG export demand, primarily by better connecting other interstate pipelines with LNG export terminals.

Two of the three major new pipeline projects in the South-Central region completed during 2021 improved natural gas delivery to Venture Global’s newly commissioned Calcasieu Pass LNG export terminal in Louisiana. These projects are as follows:

- Venture Global’s TransCameron pipeline, a 1.90-Bcf/d (54-MMcm/d), 24-mile (39-km) lateral, delivers natural gas to the terminal via interconnections with other interstate pipelines.

- Enbridge’s Cameron Extension Project, a 0.75-Bcf/d (21-MMcm/d) expansion on the Texas Eastern Transmission pipeline (TETCO), connects with the TransCameron pipeline.

The other major project in the South-Central region is the Double E pipeline, a 1.35-Bcf/d (38-MMcm/d), 135-mile (217-km) pipeline that provides new capacity from the producing areas of the Permian Basin in southeastern New Mexico to the Waha Hub in West Texas.

The Northeast had the second-most interstate natural gas pipeline capacity additions totaling 1.6 Bcf/d (45 MMcm/d) during 2021. About half of this new capacity was associated with two related projects:

- The 580-MMcf/d (16-MMcm/d) Leidy South Expansion Project on the

Transcontinental Pipeline (Transco) increased pipeline capacity from the Appalachia Basin into East Coast markets.

- The National Fuel Gas Supply Corporation’s FM 100 Project expanded its system by 330,000 cf/d (9, 345 m/d) in response to the additional Transco capacity available.

In 2021, no interstate natural gas capacity additions were added in the Southeast region, the Pacific region, the Gulf of Mexico or as part of the interconnections to Mexico.

Comments