March 2016, Vol. 243, No. 3

Web Exclusive

Why Saudi Arabia Has No Intention To End The Oil Glut

In the geopolitical and oligopolistic global oil market, purely financial supply and demand has often been a secondary force, acting when it is allowed to act. It is the strategic behavior of the producing titans, not their talk or the slow-motion supply-demand balance, which has the real power to move markets. That is the case in the last two years and remains the case in 2016.

The behavior of Saudi Arabia since 2014 has demonstrated the intent to increase both capacity and supply, a pattern not yet mitigated despite a distracting news feed from OPEC and the kingdom.

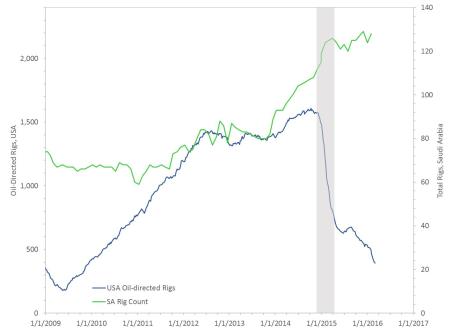

Figure 1 shows the rig counts in Saudi Arabia and the United States from 2009 to last week. (footnote: The U.S. count is oil-directed rigs while it is the total rig count in Saudi Arabia which produces mainly associated gas and exports none.) The data is shown on two different scales in such a way that the curves are equivalent during 2012 and 2013 as this was a relatively stable baseline with Saudi running 80 to 85 rigs, and 1300 to 1400 were drilling for oil in the US. What is most interesting are the actions since then.

As the shale oil revolution had sustained momentum at prices near $100 /bbl, Saudi Arabia began the second most rapid rig count expansion in its history starting in late 2013. During 2014, while the potential for oversupply was clearly known and even as prices turned sharply down in the latter half of the year, Saudi continued ramping up its rig count.

In late November 2014, the semi-annual OPEC meeting turned dissentious, and the group closed without even the pretense of a target production volume. Starting in November and continuing through March, the Saudi rig count grew in its third largest expansion in history, increasing 15 percent in four months.

At the same time, U.S. rig count was falling. Slowly at first in 2014, the rig count responded modestly to reductions in price. After the November 2014 OPEC meeting, though, the U.S. rig count began its freefall, retracing the path of the 2008 downturn. The contrast shows boldly in Figure 1. As the U.S. imploded, Saudi Arabia was ramping up.

For comparison, Saudi Arabia had a couple of times in history, though not always, reduced its rig count as the U.S. rig count dropped. Most notably, Saudi Arabia reduced then stabilized its rig count following its price war of 1986. For most of the 1990s and early 2000s the Saudi rig count tracked the same kind of pattern as the oil-directed rigs in the U.S. During the collapse of 2008-2009, Saudi Arabia again curtailed its rig count.

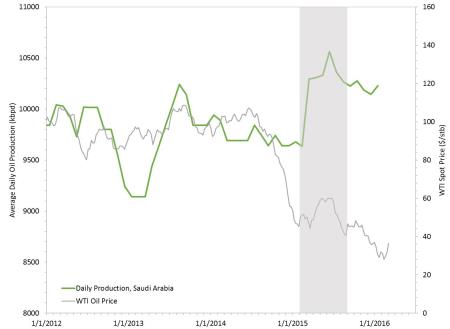

Of course, rig count alone doesn’t mean nearly as much in the Saudi command-based supply; rig count reveals more about intent and planning than current action. The real test is how the presumed increased capacity is used. Figure 2 shows that behavior, tracing Saudi production alongside oil prices. The market, presumably watching the implosion of rig count, responded by lifting WTI oil prices back into the $60s/bbl, and Saudi Arabia then responded by promptly increasing its supply, sending prices back down again. Even as prices slowly descended close to inflation-adjusted, long-term lows, the Saudi rig count slowly ramped up, and moderated its production only somewhat.

Talk of a consensus action to freeze production was rumored in January, and word of a partial agreement including Russia and Saudi Arabia hit the news in mid-February, marking the beginning of a rally in prices. It is ironic that news of a cap on further increases should be a signal for price increase in a widely oversupplied market with slow changes in demand and U.S. production. A cap on production would possibly shorten the extended period of oversupply, but certainly not alleviate it anytime soon.

Perhaps influenced by short-covering by financial speculators and perhaps influenced by dropping exchange rates for the dollar, the rally does not, in any event, mark a change to the outlook for either supply-demand fundamentals or strategic behavior of the titans. The behavior of all parties is likely to follow the thinking explained recently the Kuwaiti oil minister—if Iran doesn’t participate, then they plan to produce at full capacity. Iran has called the idea of a cap on increases “ridiculous,” and, even if they were to agree to a cap, the Saudi oil minister says rightly that there is little trust among OPEC members.

In the meantime, the rig count suggests that Saudi Arabia continues to plan for higher levels of supply. While Saudi Arabia and OPEC have talked intermittently about increasing demand and decreasing supply, about minute increases for use during Ramadan and even about the possibility of caps on production, their actions have not always comported with the distracting, laissez-faire attitude suggested by their commentary. The February rig count was only one rig shy of the kingdom’s all-time high set in December, an increase of four rigs over its January count. And its January production was higher than December by a volume roughly equal to the downward effect of all of the forces of supply and demand on U.S. production.

By Dwayne Purvis for Oilprice.com

Comments